Search Results forAirAsia X Berhad

New AirAsia X Berhad Chief Financial Officer named

Low-cost, long-haul carrier AirAsia X Berhad recently announced Wong Mee Yen as its incoming chief financial officer. Prior to AirAsia X Berhad, Wong was chief financial officer for the MRT Project of LMG Rail Car Sdn Bhd. Wong is no stranger to the airline, having been the group financial controller of AirAsia Berhad from 2004 to 2007. Her current assignment makes her responsible for corporate finance, treasury, financial planning and analysis as well as investor relations. She will report directly to Benyamin Ismail, chief executive officer of AirAsia X Berhad. ‘We are delighted to have Mee Yen on the team. Her extensive experience in financial management, strategic planning and business strategy will help to support our current business plans, company growth targets and the successful execution of key new initiatives,’ Ismail commented on the appointment. This development was also welcomed by Datuk Kamarudin Meranun, group CEO of AirAsia X. ‘We are pleased to bring back Mee Yen to join our management team at AirAsia X Berhad as we continue to drive our strategic and financial business transformation. She was part of the core team in the early days of AirAsia and has played an instrumental role in the success of AirAsia and getting the company listed on the Bursa Stock Exchange. She has vast experience in finance and operational management, and together with her intimate knowledge of AirAsia's business model, culture and products, we are confident she will be able to help us build upon our successes so far towards becoming the undisputed global long-haul low-cost carrier leader,’ he said. Wong brings with her more than 20 years of experience in finance operations and financial control. She takes over starting 01 January 2018 from Cheok Huei Shian, who has led the airline’s finance team since February 2015. “On behalf of the management team, we would like to thank Huei Shian for her invaluable contributions towards realising the company’s transformation,” Datuk Kamarudin added.

AirAsia X supports Malaysian athletes headed to the 2026 ASEAN Para Games

AirAsia X recently extended its charter service to support Malaysian athletes competing at the now-ongoing ASEAN Para Games. The airline ferried nearly 360 athletes and coaches from Kuala Lumpur to Bangkok to compete from 15th to 27th January. Operated under a special charter agreement between the National Sports Council of Malaysia and AirAsia X Berhad, this mission underscores the airline's commitment to inclusivity and national pride, ensuring the contingents travel together in comfort. AirAsia X chief executive Benyamin Ismail said of the service: "It is an honour to fly our national heroes to Bangkok. These athletes represent the best of Malaysia. Their determination, resilience and spirit inspire us all. We are proud to play our part in supporting their journey to the ASEAN Para Games”. This initiative also reflects AAX’s role beyond commercial aviation, serving as a proud partner in Malaysia’s sporting journey by championing equal opportunities for athletes at a regional stage.

Tune Protect Group Berhad triumphs at TDM Travel Trade Excellence Awards 2025 – Malaysia

The company was recognised for redefining travel insurance with the industry-first Delay Lounge Pass. Tune Protect Group Berhad emerged as the Travel Insurance Initiative of the Year winner at the TDM Travel Trade Excellence Awards 2025 - Malaysia with its Delay Lounge Pass that transforms one of air travel’s biggest frustrations: flight delays. With this first-of-its-kind initiative, insured travellers under AirAsia’s Value Pack, Premium Flex, or AirAsia Plus now enjoy automatic access to more than 1,600 airport lounges worldwide whenever their flight is delayed by two hours or more. They automatically receive a digital lounge voucher via SMS or email when their flight is delayed and can redeem it instantly at any participating lounge worldwide. If not used on the day, it remains valid for 30 days. This ease and global reach set the initiative apart, making Tune Protect a leader in experience-driven insurance solutions. Additionally, the Delay Lounge Pass uses real-time flight monitoring and automated service flows. With these, customers never need to file a manual claim. Lounge access is issued instantly, without forms, calls, or approvals. This end-to-end journey pushes the boundaries of what travel insurance can be. Instead of reacting to disruptions, Tune Protect proactively supports travellers with comfort, care, and convenience. Since the first quarter of 2025, the Delay Lounge Pass has quadrupled in growth and performance, supporting the Group’s strategy to unlock new revenue streams beyond insurance. The initiative marked an increased customer satisfaction as well by providing comfort, connectivity, and care during disruptions. On top of these, it strengthens the airline–insurer ecosystem by giving travellers a strong reason to choose insured AirAsia tickets. The Delay Lounge Pass stands as an impactful initiative that reimagines the role of travel insurance. By turning flight delays into a premium airport experience, Tune Protect has proven that insurance can evolve into a holistic part of the travel journey. The TDM Travel Trade Excellence Awards - Malaysia gives a platform to Malaysia's vibrant travel sector and applauds those who stand out across the industry. This awards programme highlights excellence in hotels, airlines, airports, cruise lines, tour operators, travel agencies, booking platforms, and travel technology. The TDM Travel Trade Excellence Awards - Malaysia 2025 is presented by Travel Daily Media Magazine. To view the full list of winners, click here. For more information on the awards programme, you may contact Danica Avila at +(65) 3158 1386 or awards@traveldailymedia.com.

AirAsia X releases financials for Q3-2025

AirAsia X Berhad reported its unaudited financial results for the third quarter ended 30th September earlier today, 28th November. The Company recorded turnover of RM803.5 million in Q3-2025, marginally higher than the RM795.0 million achieved at the end of Q3-2024. This was supported by a healthier fare environment and higher ancillary income, along with a healthy Passenger Load Factor (PLF) of 82 percent. As part of a deliberate, group-wide network optimisation to prioritise longer-haul widebody flying, the Company redeployed selected shorter and medium-haul routes, including Bangkok, Hong Kong, Amritsar and Perth, to its sister airline, which operates more cost-efficient narrowbody aircraft on these sectors. According to airline chief executive Benyamin Ismail: “The Company’s performance this quarter signals the resilience of our fare environment, driven by robust demand even during a typically softer travel period. Maintaining an 82 percent PLF was a feat and reflected the strength of our core markets and the effectiveness of the team’s continuous optimisation of our network strategy.” Key points from the quarter As a result of this strategic realignment, passengers carried declined by five percent; nonetheless, available seat kilometres were up nine percent YoY as AirAsia X lengthened average stage and improved daily aircraft utilisation to 16 hours, demonstrating the effectiveness of its focus on optimising asset productivity rather than chasing volume. Meanwhile, Revenue Passenger Kilometres rose seven percent YoY to 4,570 million, buoyed by consistently high PLF on key routes in China and Japan. Average base fare increased 5% YoY to RM466 in 3Q25 as market demand built up towards the upcoming peak travel season. Ancillary income remained an important earnings driver, up by five percent YoY to RM280.6 million as ancillary revenue per passenger rose 11 percent YoY to RM273, with duty free sales showing significant improvements against last year. Net operating profit advanced to RM12.0 million during the quarter versus RM3.0 million at the same time last year driven by favourable fuel cost and stronger local currency. Consequently, cost per ASK (CASK) dropped by nine percent YoY to 12.68 sen while CASK ex-fuel saw a modest increase of two percent to 6.72 sen. Profit after tax stood at RM27.8 million compared to RM121.6 million in 3Q24, the latter of which benefited from substantial net foreign exchange gains.

AirAsia X marks a milestone in its support of the Malaysian Battalion

AirAsia X marked yet another milestone in its history of supporting the Malaysian Battalion (MALBATT)'s mission. On Wednesday, 5th November., the airline facilitated the successful departure of its chartered flight from Sultan Abdul Aziz Shah Airport (SZB) to Beirut-Rafic Hariri International Airport (BEY), carrying 150 Malaysian Armed Forces personnel from the first group of MALBATT 850-13. Operated under a special charter agreement between the Government of Malaysia and AirAsia Berhad, this mission underscores the airline's operational capability, reliability and commitment to serving Malaysia beyond commercial operations. 13 years of proud support to the nation Now in its 13th year of supporting MALBATT peacekeeping missions, AirAsia X remains honoured to play a role in the safe and efficient deployment of Malaysian troops to Lebanon. Over the course of this year’s deployment, AirAsia X will carry a total of 532 passengers from SZB to BEY and on return flights, comprising MALBATT troops between 5, 9, 13, and 17 November. This long-standing collaboration reflects the airline’s enduring partnership with the Malaysian Armed Forces and its proud role in facilitating Malaysia’s continued contribution to international peacekeeping under the United Nations Interim Force in Lebanon (UNIFIL).

AirAsia X begins final stage of consolidation proceedings

AirAsia X Berhad announced that all conditions precedent set out in the Share Sale and Purchase Agreements (SSPAs) between AAX and Capital A Berhad have been fulfilled or waived as of Thursday, 30th October. Accordingly, as of Wednesday, 29th October,the SSPAs became unconditional in accordance with their terms and conditions. This development marks a major milestone in the proposed acquisitions of AirAsia Aviation Group Limited (AAAGL) and AirAsia Berhad (AAB), collectively forming the foundation of a consolidated airline platform under AirAsia X, which will be called AirAsia Group. This consolidated entity will be serving both medium- and short-haul routes across Asia, Australia, the Middle East, and beyond. Conditions met to the letter This latest development follows the fulfilment of all outstanding requirements. As of press time, all stakeholder consent letters and the RM1 billion private placement commitment letters for AirAsia X have been secured, along with the resolution of a regulatory exemption required from Thailand last 17th October. AirAsia X Berhad chair Fam Lee Ee said: “This is a significant step, marking AirAsia’s evolution into its next chapter. Both AirAsia and AirAsia X pioneered low-cost travel in Asia, and with the creation of AirAsia group, we are evolving that legacy to become the world’s first low-cost network carrier.” Fam added that, as the transaction is now unconditional, AirAsia Group finds itself in a better position from which to accelerate Southeast Asia’s position as a global low-cost megahub. He said: “This will boost economic multiplier benefits across the region by expanding our reach across key regions including Asia, Australia, the Middle East, and Europe. Together, we are shaping the next chapter of inclusive travel for the world.” At the same time, the consolidation will enable AirAsia Group to capture efficiencies across the value chain, from fleet and network planning to digital operations and customer experience thus creating a more agile, scalable and globally competitive low-cost airline group.

AirAsia parent firm Capital A releases Q2-2025 financials

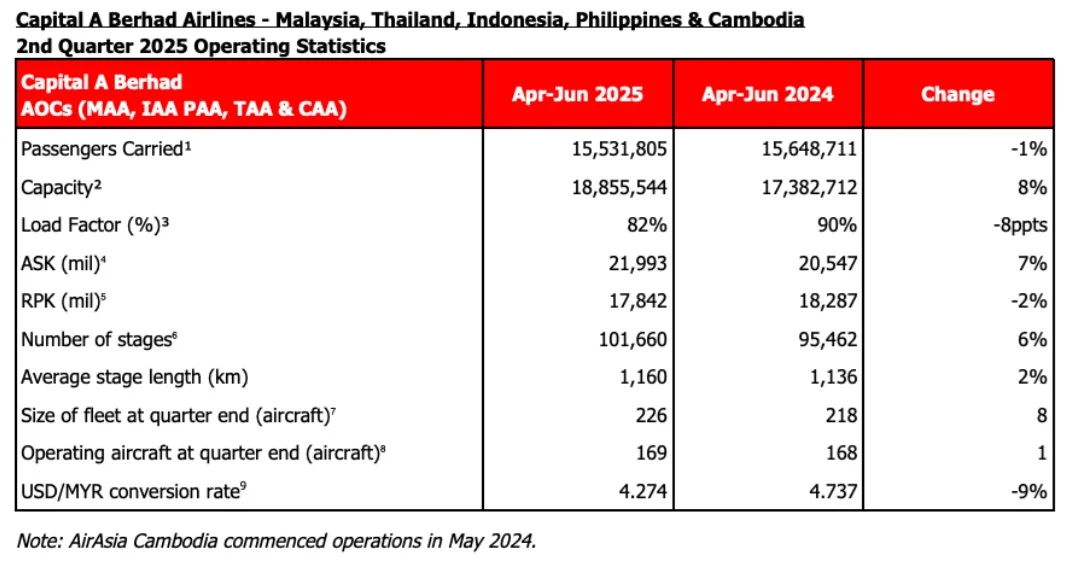

Capital A Berhad reported its unaudited financial results for the second quarter ended 30th June on Thursday, 28th August Considering how Q2 is normally considered a seasonally weak quarter, the Group recorded a revenue of RM4.8 billion, RM1.1 billion in EBITDA and Net Operating Profit of RM671 million. Profit After Tax (PAT) for the quarter was RM1.5 billion, a substantial turnaround from the RM543 million loss after taxes in Q2-2024, boosted by a RM0.9 billion foreign exchange gain. Highlights from Q2-2025 Aviation revenue dropped by three percent year-on-year (YoY) to RM 4.5 billion, largely due to weaker tourism and safety concerns in Thailand. Excluding Thailand, revenue would have increased by two percent YoY. Nevertheless, EBITDA was up 32 percent from a year ago to RM931 million, achieving a 21 percent margin, driven by lower fuel prices, stronger Asean currencies and ongoing cost optimisation. Likewise, PAT swung to RM884 million from a RM552 million loss in 2Q2024. Meanwhile, load factor held steady at 82 percent as capacity increased by eight percent YoY, while the number of passengers fell marginally by one percent YoY to 15.5 million due to softness in Thailand Likewise, average fare declined by four percent YoY to RM229, largely due to Thailand and the change of capacity mix to more domestic. Ancillary per passenger improved by two percent YoY to RM51, while ancillary revenue grew by three percent YoY, making up 19 percent of aviation revenue. This was driven by cargo revenue rising 49 percent on improved belly utilisation and better data personalisation Overall CASK fell eight percent YoY to USc4.50, largely driven by lower fuel prices and returning to a normal maintenance profile Overall fleet size grew by one aircraft to 226 aircraft, with 206 active aircraft. The executives weigh in Group CEO of AirAsia Aviation Group Bo Lingam remarked that the second quarter demonstrated the resilience of Capital A’s aviation business. Lingam said: “We offset slower demand in Thailand and lower fares from returning capacity with disciplined cost management and strong ancillary growth, supported by favourable fuel and forex trends. Load factor remains high as we bring capacity back online and align supply with market needs. Core short-haul demand held firm, boosted by the summer peak in North Asia, regional festivities and long weekends in Malaysia and other key markets.” He further expressed confidence that this momentum will carry into the second half, with the fourth quarter historically being the airline business’ strongest. With regard to AirAsia’s Thai market, Lingam said: “Thailand remains an important market for us, and we intend to hold our market share, especially domestically, at 40 percent through targeted capacity redeployment into domestic and to India, as well as refined pricing strategies. We are expecting Thailand to see a rebound from the fourth quarter onwards.” For his part, Capital A chief executive Tony Fernandes lauded the company for delivering strong results in what is usually their weakest quarter. Fernandes enthused: “Aviation’s back on track, and we’re close to returning to our full fleet strength. Add to that, almost all our Capital A Companies are profitable at PAT level, and we have strong earnings potential. Now that we’ve steadied the ship, it’s all about growth.” The chief executive added that the goal for the next six months is for the company to get all its aircraft back, grow its operations in the Philippines and Indonesia, and return the share of AirAsia on MOVE to 60 percent in order to grow ancillary revenue. At present, the company is currently working on a rated bond and securing local debt to restructure its COVID-era financing which dragged down its profits. Fernandes added: “On the aviation disposal, we are on the last leg of restructuring. At the moment, we’re in the process of responding to some feedback from the Thai SEC, and we hope to resolve any outstanding matters soon.”

AirAsia X announces financial results for Q2-2025

AirAsia X Berhad reported its unaudited financial results for the second quarter ended 30th June on Tuesday, 26th August. The Company recorded a turnover of RM660.8 million in the second quarter of the year, marginally lower year-on-year as capacity rose by six percent YoY to 1.12 million seats in a softer fare environment due to low season. Passenger traffic grew by six percent YoY to 935,105 passengers, maintaining a sound Passenger Load Factor (PLF) of 83 percent, unchanged YoY despite the increased capacity. According to AirAsia X CEO Benyamin Ismail: "AirAsia X delivered resilient performance this quarter with a sound PLF of 83%, in line with capacity growth despite the seasonally softer second quarter. The Group’s operations remained profitable even as one aircraft is pending reactivation and fares are softer as the market tries to boost demand taking advantage of the lower fuel price environment in 2Q25.” Ismail added that the final aircraft reactivation which was initially scheduled for June was deferred to the second half of the year due to the well-documented global MRO backlogs and spare parts shortages. Also, as of 30th June, AirAsia X’s total fleet stood at 19 A330 aircraft; of these, 18 aircraft are active and operational. Fares and revenue This quarter, average base fare declined to RM405, impacted by historical seasonality and cautious travel sentiments following the concerns on earthquakes in Japan. In managing seasonality, the Company had also augmented its load-active, yield-passive strategy, leveraging on the advantageous fuel price environment. Ancillary revenue bolstered the Company’s performance with revenue per passenger up by four percent YoY to RM257 and total ancillary revenue rising by ten percent YoY, driven by higher passenger volumes and enhanced product offerings particularly in the duty free and merchandise segments. Profit in Q2-2025 Net profit rose sharply to RM35.22 million against last year’s RM4.82 million, boosted by favourable net foreign exchange gains. In the second quarter, the Company’s net operating profit improved 26 percent YoY to RM1.38 million supported by lower fuel prices. The Company’s cost per available-seat-kilometres (ASK / CASK) fell by 13 percent YoY to 12.05 sen while CASK ex-fuel stood at 6.38 sen, up by nine percent YoY reflecting operational ramp-up and higher maintenance expenses over the last 12 months. In terms of capacity and network, the Company’s ASK grew by ten percent YoY to 4,851 millions as AirAsia X continued to observe strong PLF of beyond 85 percent from its East Asian routes in Japan, China and South Korea driven by the peak spring travel season during the quarter. Associate performance in Q2-2025 Company associate AirAsia X Thailand (TAAX) posted a revenue of RM372.82 million and an operating loss of RM13.2 million in Q2-2025. Passenger traffic during the quarter declined by 12 percent YoY to 318,257 passengers as seat capacity reduced by five percent YoY to 407,360 seats. TAAX’s PLF stood at 78 percent this quarter as performance was pressured by softened travel demand to Thailand overall following the earthquake incident in Bangkok and related security concerns. Average fare was firm at RM690 during the quarter under review, and TAAX posted a net profit of RM10.58 million, buoyed by net foreign exchange gains. TAAX maintained a fleet of nine A330s after returning one aircraft to lessor during the quarter.

AirAsia to change the game yet again with purchase order for 50 Airbus A321XLRs

AirAsia Berhad signed a landmark agreement with Airbus for the purchase of 50 A321XLRs on Saturday, 5th July. The signing in Paris between Capital A chief executive Tony Fernandes and his counterpart at Airbus Commercial Aircraft Christian Scherer was witnessed by Malaysian Prime Minister of Malaysia Anwar Ibrahim. The purchase’s total value is at US$12.25 billion and also includes rights for 20 A321XLRs, and the aircraft are scheduled for delivery between 2028 and 2032. With this agreement, the airline takes a major step towards becoming the world’s first low-cost narrow-body network carrier, anchored by its multi-hub strategy. Taking Asian aviation to the next level. Fernandes pointed out that AirAsia pioneered low-cost travel and Asia and is now set to take the sector to the next level. He said: “AirAsia is on a transformative journey to become the world’s first low-cost network carrier. This is about exponential growth, connecting geographies beyond Asean, and making flying even more democratic. We gave people in ASEAN the opportunity to explore Asia; now, we want the world to see ASEAN, and ASEAN to see the world. The A321XLR and A321LR are the game-changers enabling this vision, and we are proud to lead the charge in making our world smaller. We can’t wait to paint the skies even wider in red.” For his part, Scherer expressed pleasure over the confirmation of the agreement, as well as over becoming part of the next phase of AirAsia’s development. Scherer said: “Having resumed its growth trajectory, which we salute and support, AirAsia is creating solid fleet efficiencies, allowing global network expansion. The A321XLR unlocks new opportunities for AirAsia to launch non-stop flights linking primary and secondary cities all around the globe.” The next-generation A321XLRs will operate alongside AirAsia’s all-Airbus fleet of A320 Family and A330 aircraft, supporting its long-term strategy to deliver unmatched connectivity across Asia and beyond, whilst maintaining a low-cost model through improved route economics, enhanced aircraft utilisation and fleet efficiency. AirAsia Group aims to carry 150 million guests annually by 2030, reaching a cumulative total of 1.5 billion guests since inception. The new fleet plays a pivotal role in this transformation as AirAsia’s multi-aircraft strategy enables the airline to match capacity with demand, reduce fuel consumption, and support a sustainable, cost-effective growth model in a highly competitive global landscape. The A321XLR also offers up to 20 percent lower fuel burn per seat than the Airbus A321neo aircraft, significantly improving emissions performance and operating efficiency.

AirAsia X releases financials for Q1-2025

AirAsia X Berhad released its financial report on 28th May, detailing its progress in the three-month period that ended 31st March. AirAsia X reported a revenue of RM940.1 million in the first quarter of this year, up by three percent year-on-year from the RM908.9 million total reported for the same period in 2024. This increase was driven by a 12 percent growth in capacity to 1.29 million seats. Likewise, in line with capacity expansion, AirAsia X achieved a 12 percent YoY increase in passenger traffic in Q1-2025, carrying 1.08 million passengers. The increase in passenger traffic was driven by sustained demand across core markets and efficient capacity deployment, resulting in a robust Passenger Load Factor of 83 percent. Relevant developments for the quarter This quarter, average base fare stood at RM550, aligning with the Company’s load-active, yield-passive strategy. Ancillary revenue remained a key margin driver in Q1-2025, with ancillary revenue per passenger rising ten percent YoY to RM277. This uplift, combined with a higher passenger base, drove a 24 percent YoY increase in total ancillary revenue to RM298.3 million. The growth reflects improved takeup rates, supported by enhanced digital personalisation and targeted product offerings that successfully maximised per-passenger spend. AirAsia X also posted a net profit of RM50.2 million, representing a five percent margin even as its cost base expanded parallel to operational growth. Cost per ASK edged up marginally to 13.97, driven by slightly higher staffing with additional aircraft in operation and airport-related expenses. These were partially mitigated by a lower jet fuel price YoY and a reduction in aircraft lease expenses as most aircraft exited pay-by-hour arrangements since Q1-2024. During the first quarter, AirAsia X expanded its Available Seat Kilometres by 17 percent YoY to 5,878 million, strategically aligning capacity to capture peak demand during festive and holiday periods. Japan and Australia emerged as key outperformers within the network, with core routes delivering strong load factors between 85 and 90 percent, reflecting sustained travel demand and effective capacity optimisation in high-yield markets. Progress among associates AirAsia X Thailand (TAAX) recorded RM512.7 million in revenue and an operating profit of RM15.5 million in the first quarter. TAAX carried a total of 500,128 passengers this quarter, up 14 percent YoY as seat capacity increased by 23 percent YoY to 604,584 seats, charting a sound PLF of 83 percent during the quarter. The one-off effect of the hub transition from Suvarnabhumi to Don Mueang in October 2024 has stabilised, with the network now operating at peak performance. TAAX’s average fare held strong at RM833 per passenger this quarter. As of 31st March, AirAsia X’s total fleet now stands at 19 A330 aircraft following the induction of one additional aircraft from a third-party lessor. Of these, 17 aircraft were activated and operational, and TAAX maintained a fleet of ten A330s, supporting network recovery and growth across core markets.

No companies found matching your search.

Return To HomeNo Event found matching your search.

Return To Home