The International Air Transport Association (IATA) announced strong demand growth in air travel for March 2023.

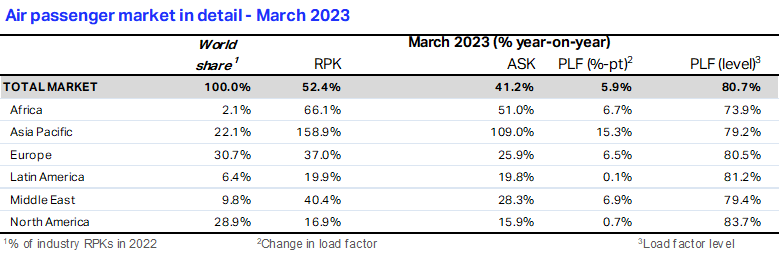

- Total traffic in March 2023 (measured in revenue passenger kilometers or RPKs) rose 52.4% compared to March 2022. Globally, traffic is now at 88.0% of March 2019 levels.

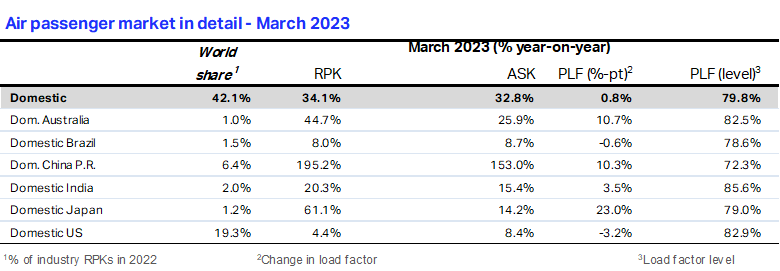

- Domestic traffic for March rose 34.1% compared to the year-ago period. Total March 2023 domestic traffic was at 98.9% of the March 2019 level.

- International traffic climbed 68.9% versus March 2022 with all markets recording healthy growth, led once again by carriers in the Asia-Pacific region. International RPKs reached 81.6% of March 2019 levels while the load factor at 81.3% exceeded the March 2019 level by 10.1 percentage points.

“The calendar year first quarter ended on a strong note for air travel demand. Domestic markets have been near their pre-pandemic levels for months. And for international travel two key waypoints were topped. First, demand increased by 3.5 percentage points compared to the previous month’s growth, to reach 81.6% of pre-COVID levels. This was led by a near-tripling of demand for Asia-Pacific carriers as China’s re-opening took hold. And efficiency is improving as international load factors reached 81.3%. Even more importantly, ticket sales for both domestic and international travel give every indication that strong growth will continue into the peak Northern Hemisphere summer travel season,” said Willie Walsh, IATA’s Director General.

International Passenger Markets

Asia-Pacific airlines had a 283.1% increase in March 2023 traffic compared to March 2022, continuing the robust momentum since the lifting of travel restrictions in the region. Capacity rose 161.5% and the load factor increased 26.8 percentage points to 84.5%, the second highest among the regions.

European carriers posted a 38.5% traffic rise versus March 2022. Capacity climbed 27.0%, and load factor rose 6.6 percentage points to 79.4%, which was the second lowest among the regions.

Middle Eastern airlines saw a 43.1% traffic increase compared to March a year ago. Capacity climbed 30.5% and load factor pushed up 7.0 percentage points to 79.4%.

North American carriers’ traffic climbed 51.6% in March 2023 versus the 2022 period. Capacity increased 34.0%, and load factor rose 9.8 percentage points to 84.8%, the highest among the regions.

Latin American airlines had a 36.5% traffic increase compared to the same month in 2022. March capacity climbed 33.4% and load factor rose 1.9 percentage points to 82.8%.

African airlines’ traffic rose 71.7% in March 2023 versus a year ago, the second highest among the regions. March capacity was up 56.2% and load factor climbed 6.5 percentage points to 72.2%, lowest among the regions.

Domestic Passenger Markets

Brazil’s domestic traffic rose 8.0% in March compared to a year ago and is now just fractionally below pre-pandemic levels.

Indian airlines’ domestic demand climbed 20.3% in March and was 10.0% above the March 2019 levels.

The Bottom Line

“As traveler expectations build towards the peak Northern Hemisphere summer travel season, airlines are doing their best to meet the desire and need to fly. Unfortunately, a lack of capacity means that some of those travelers may be disappointed. Part of this capacity shortfall is attributable to the widely reported labor shortages impacting many parts of the aviation value chain, as well as supply chain issues affecting the aircraft manufacturing sector that is resulting in aircraft delivery delays. However, a significant share of recent flight cancellations, primarily in Europe, are owing to job actions by air traffic controllers and others. These irresponsible actions resulted in thousands of unnecessary cancellations in March. This is unacceptable and should not be tolerated by the authorities,” said Walsh.

Comments are closed.